Why Coordinated Social Security and Dubai-Focused Wealth Planning Matters for Expat Retirement

Planning for retirement can feel like a big puzzle, especially when you live in a different country than where your Social Security benefits come from. Many people get advice on their Social Security rules, then separate advice on cross-border tax issues, and even more advice on things like buying property in Dubai. This way of doing things means you’re often getting fragmented advice, where no one sees the whole picture of your money.

Think of it this way: your Social Security income, your taxes as an expat, and your investments in Dubai property are all parts of one big retirement plan. But if you talk to different people for each part, it’s hard to make sure everything works well together. This is a common challenge for expats, as managing money across different countries is quite complex Cross-Border Financial Planning: What You Need to Know.

The good news is, there’s a better way. This guide will show you how working with a specialized financial advisor can bring all these parts together. A smart financial advisor for Social Security can help you understand your benefits, while also connecting them to your personal financial planning in a global way. They can offer advice on financial planning that includes your wealth management in Dubai, like property opportunities, to make your retirement much better.

Imagine having a chief financial advisor who looks at your Social Security benefits, your Dubai investments, and your overall financial health all at once. This kind of integrated approach helps you make smarter choices, leading to a more secure and joyful retirement. We’ll explore how to find such an expert and what questions to ask when you’re considering how to choose a fiduciary financial advisor Dubai for property.

Are you buying, selling, renting, or investing in Dubai? Connect with Ayaz Salman for Free Consultation.

FREE Dubai Real Estate Consultation

1) Why Expat Retirement Planning Must Include Social Security and Local Property Strategy

For many expats, their Social Security benefits from their home country are a very important part of their retirement money. These benefits, along with other retirement income from back home, often form the strong base of their plan. It’s like the solid ground your retirement house is built on. However, living abroad adds special layers to this foundation. You can’t just think about your Social Security in a bubble.

When you’re an expat in a place like Dubai, local property investments can play a big role in your retirement. Many people buy property in Dubai not just to live in it, but also as a way to grow their wealth.

Buying property can also help you get an investor residency visa, which means you can live in Dubai for a longer time. For example, recent rules from 2026 may make it easier to get a two-year real estate investor residency visa, sometimes with a minimum property value of AED 750,000 GMS Flash Alert 2026-125: United Arab Emirates – KPMG International. These property investments and residency options become key parts of your overall personal financial planning.

The trick is making sure your Social Security benefits and your Dubai property strategy work together smoothly. If they don’t, you might face some unexpected problems. You could find yourself with less money than you thought, or run into tricky tax situations in different countries. This is why you need advice on financial planning that connects all the dots.

A good financial advisor for Social Security understands how your benefits fit into a bigger, global picture. They can help you see how your wealth management Dubai efforts, like investing in apartments or other properties, connect with your Social Security income. This integrated approach helps you avoid shortfalls and makes sure your money works as hard as it can for you. For insights into smart property choices, explore Sunset Apartments Dubai: Buy, Rent, or Invest Smarter in 2026.

Having a chief financial advisor who can guide you through both your home-country benefits and your local investments means your retirement plan is strong and clear, no matter where you choose to live.

2) Understanding Social Security for Expats: Totalization Agreements, Eligibility, and Claiming Rules

You’ve learned that your Social Security from back home and your property investments in places like Dubai need to work together for a strong retirement. But what about the nuts and bolts of Social Security itself when you’re living far away? It’s not always as simple as it sounds.

For expats, understanding how your Social Security benefits truly work is very important. This includes knowing about special rules like totalization agreements, how your past work counts, and when and where you can claim your money. This is where a good financial advisor for social security really helps.

What are Totalization Agreements?

Imagine you’ve worked in both your home country and another country during your life. Without a special agreement, you might not have paid into either country’s social security system enough to get benefits from either one. That’s a problem!

Totalization agreements are like special handshakes between countries. They stop you from losing out on benefits because you’ve worked in different places. These agreements help by letting you combine your work periods from two countries to meet the minimum time needed to qualify for Social Security. This means your work in a foreign country can count towards getting your benefits, and vice versa. Many countries have these agreements in place to help migrant workers secure their retirement Improving Social Insurance for Migrants.

The U.S. Social Security Administration, for example, has agreements with several countries to avoid double taxation and to help people get benefits they might otherwise lose. In 2026, these agreements continue to be a key part of international Social Security planning. The Social Security Administration even oversees data-sharing agreements related to these totalization agreements FY 2026 Congressional Justification Table of Contents.

Eligibility and How Residency Affects Claims

Your eligibility for Social Security benefits mostly depends on how much you’ve paid into the system through your work. This is usually measured in "credits." Most people need 40 credits to get retirement benefits.

When you live abroad, especially if your home country has a totalization agreement with the country you are living in, your work periods can be combined. This helps you reach those needed credits. But your eligibility can also depend on your citizenship and where you live. For example, some countries might have rules about how long you can receive benefits if you move out of their borders permanently.

Residency plays a big part in claiming rules.

- Receiving benefits abroad: You can often receive your Social Security benefits while living overseas. However, rules can vary. Some countries might have specific requirements.

- Taxation: Your benefits might be taxed differently depending on the tax agreements between your home country and your country of residence. This is a big area where good personal financial planning comes in handy.

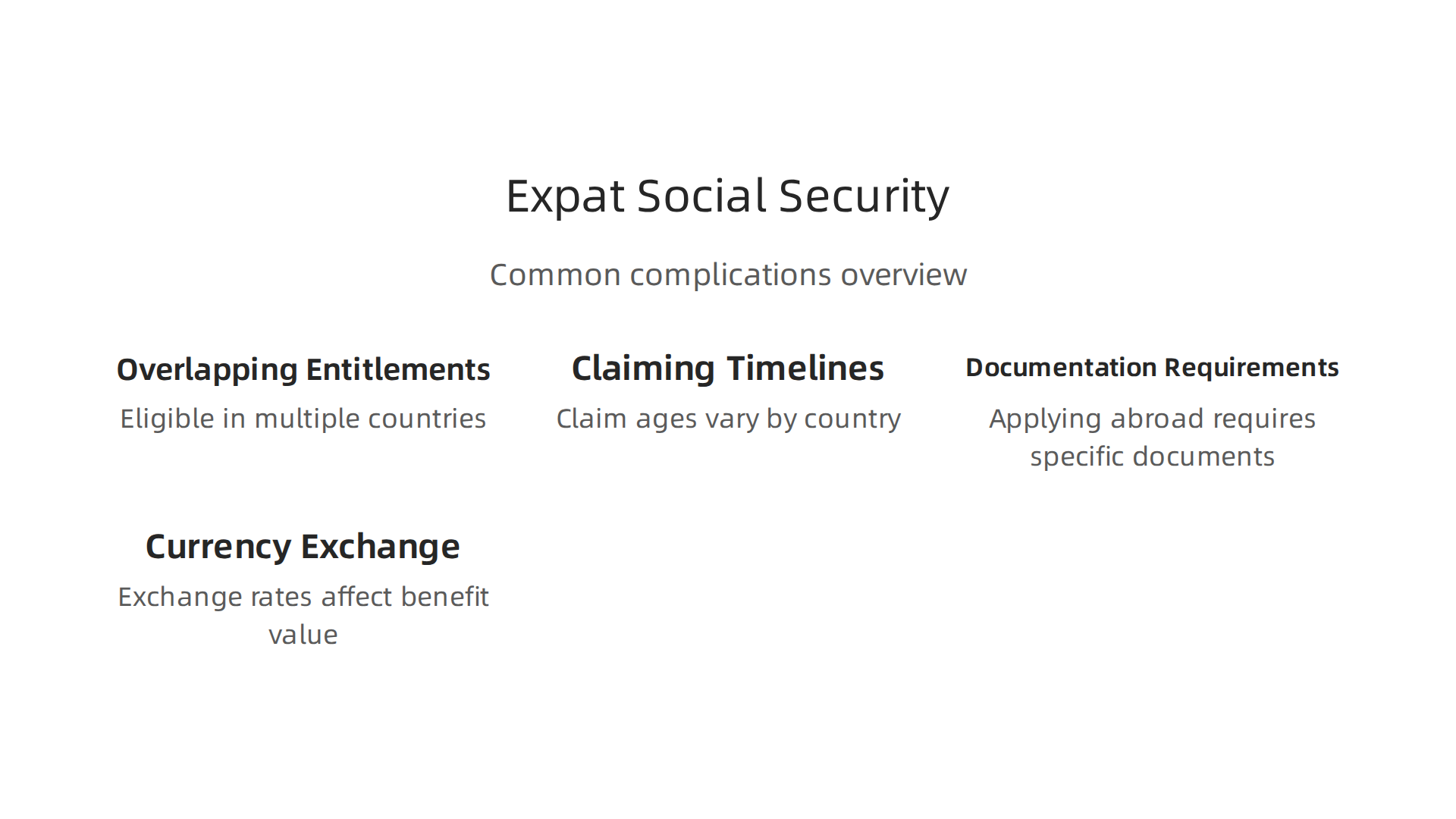

Common Complications for Expats

Navigating Social Security as an expat can come with its own set of challenges:

- Overlapping Entitlements: Sometimes, you might be eligible for social security benefits from more than one country. Knowing which one to claim first, or how they might affect each other, can be tricky.

- Claiming Timelines: The age you can claim benefits might be different in various countries. Missing a deadline or claiming too early could mean less money over time.

- Documentation Requirements: Applying for benefits from abroad often means gathering specific documents, proving your identity, and dealing with international mail or online systems. This can be complex and time-consuming.

- Currency Exchange: Fluctuations in currency rates can impact the actual value of your benefits when converted to the local currency where you live.

This is why getting solid advice on financial planning is essential. A specialized chief financial advisor who understands expat finances can help you untangle these complexities. They will make sure you get all the benefits you’re entitled to and that your Social Security fits perfectly into your larger wealth management Dubai plan.

It’s clear that dealing with Social Security when you’re an expat can be tricky. This is where a skilled financial advisor comes in. They don’t just look at your Social Security by itself. They see it as one important part of your whole money picture.

This includes your pensions, savings, investments (like property in Dubai), and how much money you need each month. A good financial advisor for social security helps put all these pieces together. This is called cross-border financial planning, which is very important for people living in different countries in 2026.

How Advisors Model Your Retirement Income

Advisors use special tools to see how your money will last throughout your retirement. They look at different "what if" situations. For example, what if you claim Social Security earlier or later? What if your investments grow more or less than expected?

They also think about "longevity risk." This is the chance that you might live longer than your money lasts. A financial advisor helps you plan so your money can support you for many years, even into old age How Do Retirement Investors and Financial Advisors View and Cope with Policy Risk?. They also help you figure out your "replacement rate." This means how much of your working income your retirement funds will replace, giving you a clear picture of your future financial comfort.

Coordinating Benefits with Investments and Property Income

For expats, this part can be extra tricky. You might have Social Security from your home country, a pension from another, and rental income from property you own in Dubai. A dedicated financial advisor for social security helps you plan exactly when to take money from each source. This smart planning can help you pay less in taxes and make your money last longer. They can help you decide if it’s better to take Social Security first, or draw from your investments, or use your rental income. Bringing all these different parts together is a key job for someone doing wealth management Dubai.

Tools and Best Practices Advisors Use

Advisors use advanced computer programs to create a financial roadmap just for you. This roadmap shows how your money flows in and out over time, helping you visualize your financial future. They also stay up-to-date with the latest rules for taxes and Social Security in various countries. In 2026, advisors are focusing on being true partners who help with your overall well-being and managing financial risks Three Shifts Defining the Retirement Advisor’s Role in 2026.

They help you avoid common mistakes, like taking benefits at the wrong time or not planning for currency changes. Finding a trustworthy advisor, especially one who acts as a fiduciary, is very important. A fiduciary always puts your best interests first Choosing a Financial Advisor in 2026. This is a top best practice in personal financial planning.

If you’re an expat with property in Dubai, understanding how your rental income fits into this bigger picture is crucial. A financial advisor can help you manage your apartments for rent in Dubai UAE 2026 while making sure your Social Security and other pensions work together seamlessly. Ultimately, their role is to give you peace of mind that all your hard-earned money will support your life goals, no matter where you choose to live.

4) Using Dubai Real Estate and Investor Residency as Part of a Retirement Strategy

When planning your retirement as an expat, especially if you’re thinking about wealth management Dubai, putting your money into property can be a very smart move. Dubai real estate offers several ways to help your retirement fund grow.

How Property Can Make You Money for Retirement

There are a few main ways property in Dubai can help your retirement:

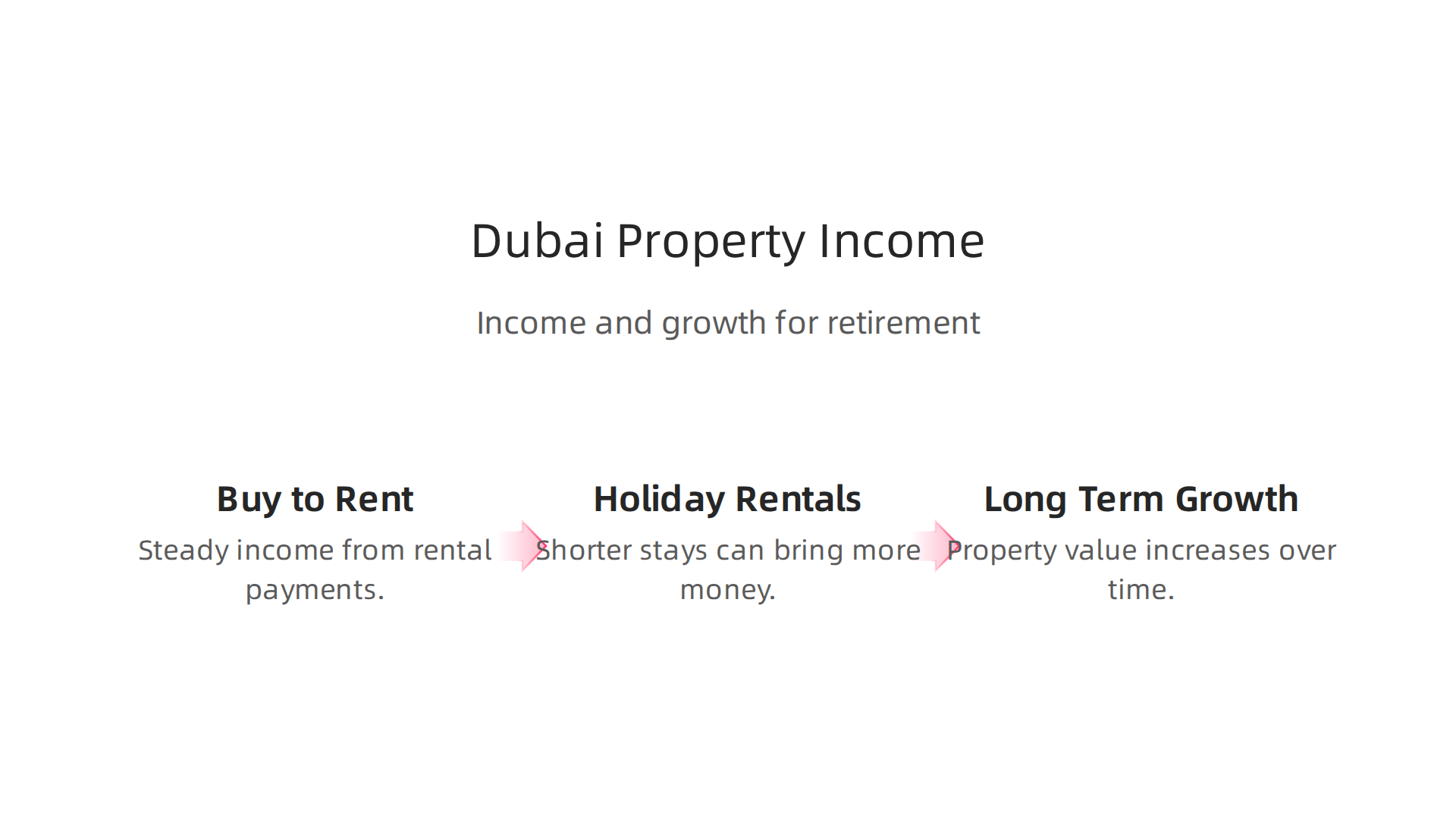

- Buying to Rent (Buy-to-Let): This is when you buy a home or apartment and then rent it out to others. The money you get from rent each month can be a steady income for your retirement. In 2026, Dubai properties are still known for giving good rental returns compared to many other big cities. For example, some apartments can offer a net yield of 3-5% in 2026, depending on where they are located Dubai Rental Yield 2026: 3–5% Net Returns. This kind of passive income can greatly support your living costs later in life. You can learn more in this your 2026 guide to apartments to rent in Dubai.

- Holiday Rentals: Instead of long-term renters, you can rent out your property to tourists for shorter stays, like a vacation home. This can sometimes bring in even more money, especially in popular areas.

- Long-Term Growth: Over time, the value of your property itself can go up. This is called capital appreciation. When you sell it later, you might make a profit, which adds to your retirement savings. The Dubai real estate market 2026: Rental yields, prices & what’s next shows that the market remains strong.

Investor Residency and Your Retirement

Another big benefit of buying property in Dubai is that it can help you get an investor residency visa. This visa lets you live in Dubai for a long time, which is perfect for retirement.

- How it Works: The Dubai government has rules that let people who invest a certain amount in property get a residency visa. For example, a property investment of 2 million AED (about 545,000 USD) or more can often get you a longer residency visa GLMM Policy Brief. There are also often options for smaller investments, like AED 750,000 for a two-year visa, with updated rules changing eligibility [GMS Flash Alert 2026-125: United Arab Emirates – KPMG International].

- Retirement Freedom: Having an investor residency visa gives you a lot of freedom. You can easily travel in and out of Dubai, open bank accounts, and access local services. This means you can enjoy your retirement in a vibrant, tax-friendly city with fewer worries about immigration paperwork. It offers flexibility to live where you want, for as long as you want, during your golden years.

Putting real estate into your overall personal financial planning can be a smart move, especially when you think about income from rent and the chance of getting residency. It’s wise to get expert advice on financial planning to make sure your property investments and residency plans work together well.

Buying, selling, renting, or investing in Dubai? Connect with Ayaz Salman for a FREE Dubai Real Estate Consultation.

Navigating your retirement plans with Dubai assets means you also need to understand the important rules about taxes and reporting. While Dubai is known for its tax-friendly environment, your home country may still have rules you need to follow, especially when it comes to things like Social Security and income from your property. This is why getting professional advice on financial planning is so important.

Understanding Tax and Reporting for Dubai Assets

When you own property in Dubai and are an expat, you have to think about two sets of rules: those in the UAE and those in your home country.

- Dubai’s Tax Rules for Property: A great thing about Dubai is that there is generally no personal income tax. This means the money you earn from renting out your Dubai property usually isn’t taxed in the UAE. Also, there are no capital gains taxes when you sell property here. This makes wealth management Dubai very appealing.

- Your Home Country’s Tax Rules: Here’s the catch: most countries expect their citizens or long-term residents to report their worldwide income. So, even if your rental income from Dubai isn’t taxed there, you might still need to report it and pay taxes on it in your home country. This can be complex, and you might need a financial advisor for social security and international taxes. They can help you understand these global obligations as part of your overall personal financial planning.

Social Security and Cross-Border Considerations

For expats, how your Social Security benefits work with your overseas assets and income is another key area.

- Totalization Agreements: Some countries have special deals with the United States called Totalization Agreements. These agreements stop people from having to pay Social Security taxes in two countries on the same earnings. They also help workers from one country count their work years in another country to meet the minimum time needed to get Social Security benefits. For example, some foreign employees might be exempt from local Social Security payments if their home country has such an agreement Doing Business in Latin America 2025 – 2026 | EY. It’s important to check if your home country has one of these agreements with the country you worked in or are receiving benefits from.

- Reporting Foreign Accounts: If you have bank accounts in Dubai for your rental income, you might need to report these to your home country’s tax authority. For example, U.S. citizens often need to file an FBAR (Report of Foreign Bank and Financial Accounts) if their foreign accounts meet a certain value.

Avoiding Double Taxation

The good news is that many countries have tax treaties with each other to prevent you from paying tax twice on the same income. These treaties outline which country has the right to tax different types of income. Your financial advisor, especially one who understands international tax laws, can help you use these treaties to your advantage, making sure your Dubai assets fit smoothly into your retirement plan.

Managing your money across borders needs careful planning. A good chief financial advisor can guide you through these complex rules, ensuring your Dubai property investments help your retirement without unexpected tax issues.

6) How to Choose a Financial Advisor Who Understands Social Security and Dubai’s Market

Finding the right expert to help with your money when you have assets in Dubai and want to plan for retirement, especially with Social Security in mind, is very important. You need someone who knows both your home country’s rules and Dubai’s special market. This isn’t just about finding any financial helper; it’s about finding a financial advisor for social security who truly understands the bigger picture.

What Makes a Good Financial Advisor for Expats?

When you look for a financial advisor, especially one who can help with your Dubai properties and Social Security, keep these key things in mind:

- Proper Training and Standards: Look for an advisor who is a "fiduciary." This means they must always put your best interests first, even before their own. Advisors who follow this rule, like Certified Financial Planners (CFP® professionals), have strict guidelines to follow, making sure their advice is honest and loyal to you. The U.S. Department of Labor also stresses the importance of advisors meeting proper standards of care for retirement investors in 2026. You can learn more about finding a good advisor by looking for one who upholds strong standards of conduct and ethics.

- Experience with Different Countries: Your advisor needs to know about cross-border money matters. This means they understand how taxes work between your home country and the UAE. They should also be familiar with how Social Security works for people living overseas, including special deals between countries called Totalization Agreements. A cross-border investment advisor is specifically trained to help clients manage money across different countries, looking at tax rules and reporting needs.

- Track Record with Expats: Ask them if they have helped other people like you, especially those living abroad and owning property in places like Dubai. Their past work with expats shows they know the common challenges and how to help solve them.

Important Questions to Ask Your Advisor

When you meet with potential advisors, ask these questions to see if they are the right fit for your unique situation:

- "What is your experience with Totalization Agreements?" These agreements can greatly affect how your Social Security benefits are taxed or if you need to pay into different systems. An advisor who understands how these agreements work can save you a lot of trouble.

- "How do you help coordinate taxes between my home country and the UAE?" You want an advisor who can help you avoid paying taxes twice on the same income and make sure you follow all the rules in both places. This is a big part of sound

personal financial planningfor expats. - "Can you advise on structuring real estate for investment and residency?" If you are using your Dubai property to get a residency visa, your advisor should know the latest rules for these investor programs. For example, Dubai has updated rules that may expand eligibility for its two-year real estate investor residency visa.

- "Do you offer

advice on financial planningthat includes residency planning?" Beyond just taxes, a goodchief financial advisorshould think about how your property and financial choices affect your ability to live and work in Dubai long-term.

Choosing the right financial advisor for social security and your Dubai assets means you’ll have a guide to help you make smart choices, manage your wealth, and enjoy your retirement plans without worries. This kind of specialized wealth management Dubai is truly invaluable.

If you’re looking to make smart moves with your Dubai property, whether buying, selling, renting, or investing, getting expert help is key.

Connect with Ayaz Salman for a FREE Dubai Real Estate Consultation.

Getting the right financial advisor for social security and your Dubai wealth is the first big step. Now, let’s look at how these experts put together a clear plan for your future. They don’t just talk; they show you what a successful retirement might look like with real examples, helping you see how all your money parts fit together.

How Advisors Build Your Retirement Plan

A good chief financial advisor helps you mix all your different types of income. This includes your Social Security benefits, any pensions you might have, money from your other investments, and the cash you get from renting out your property in Dubai. Think of it like a puzzle where each piece is a part of your money. Your advisor helps put them all in the right place for a full picture. This is a big part of smart personal financial planning when you live across borders.

For example, imagine a couple, Maria and David, living in Dubai. Their financial advisor for social security helps them map out a plan:

- Social Security: They decide when to start taking their Social Security payments.

- Pensions: Their advisor shows how their old work pensions will add to their monthly income.

- Investments: Money from stocks and bonds fills in the gaps, making sure they have enough for their everyday life and fun activities.

- Dubai Rental Income: Their apartment in Dubai brings in steady cash. In 2026, Dubai properties continue to offer good rental returns, often around 3-5% net, which can be a strong part of a retirement income plan. This is a key part of

wealth management Dubai. You can learn more about the market and its yields in the Dubai real estate market 2026: Rental yields, prices & what’s next report.

This kind of detailed advice on financial planning helps them feel safe and ready for the future, knowing their money works for them no matter where they are.

This kind of planning, spanning across different countries, is known as Cross-Border Retirement Planning: What You Need to Know.

Big Decisions for Your Retirement Plan

When creating your plan, a financial advisor for social security will help you think through some important choices:

- When to Claim Social Security: This is a huge decision. Should you start taking payments early, or wait until your full retirement age for bigger checks? Your advisor can show you how each choice affects your total income over time.

- What to Do with Your Dubai Property: Your advisor will help you decide if it’s better to keep renting out your property for income, sell it to get a lump sum of money, or even use it as a guarantee for a loan. This decision ties directly into your cash flow and overall

wealth management Dubai. For more help on finding the right expert, read about How to Choose a Fiduciary Financial Advisor Dubai for Property. - Residency Choices: Your property in Dubai can also affect your right to live there. Your advisor will help you understand how your property choices fit with Dubai’s rules for residency visas, especially if you want to stay in the UAE for the long term.

These choices are not always easy, but with good personal financial planning and a knowledgeable advisor, you can make the best decisions for your future. It really helps expats and investors unlock their wealth, and grow their financial literacy for investors and expats.

Summary

This article explains why expat retirement planning works best when Social Security, cross‑border tax rules, and Dubai property strategies are coordinated rather than handled separately. It covers how totalization agreements, eligibility rules, and claiming timelines affect benefits, and shows how rental income or investor residency in Dubai can bolster retirement cash flow. You’ll learn practical risks—like taxation at home, currency exposure, and documentation demands—and how advisors model retirement outcomes to manage longevity and policy risk. The guide describes best practices for choosing a fiduciary advisor with cross‑border experience, questions to ask, and how property can supply rent, capital gains, or residency. By the end you’ll know how to align Social Security with Dubai investments to reduce surprises and make your retirement plan more durable and tax‑efficient.